GlobalFoundries Stops All 7nm Development: Opts To Focus on Specialized Processes

by Anton Shilov & Ian Cutress on August 27, 2018 4:01 PM EST- Posted in

- Semiconductors

- CPUs

- AMD

- GlobalFoundries

- 7nm

- 7LP

GlobalFoundries on Monday announced an important strategy shift. The contract maker of semiconductors decided to cease development of bleeding edge manufacturing technologies and stop all work on its 7LP (7 nm) fabrication processes, which will not be used for any client. Instead, the company will focus on specialized process technologies for clients in emerging high-growth markets. These technologies will initially be based on the company’s 14LPP/12LP platform and will include RF, embedded memory, and low power features. Because of the strategy shift, GF will cut 5% of its staff as well as renegotiate its WSA and IP-related deals with AMD and IBM. In a bid to understand more what is going on, we sat down with Gary Patton, CTO of GlobalFoundries.

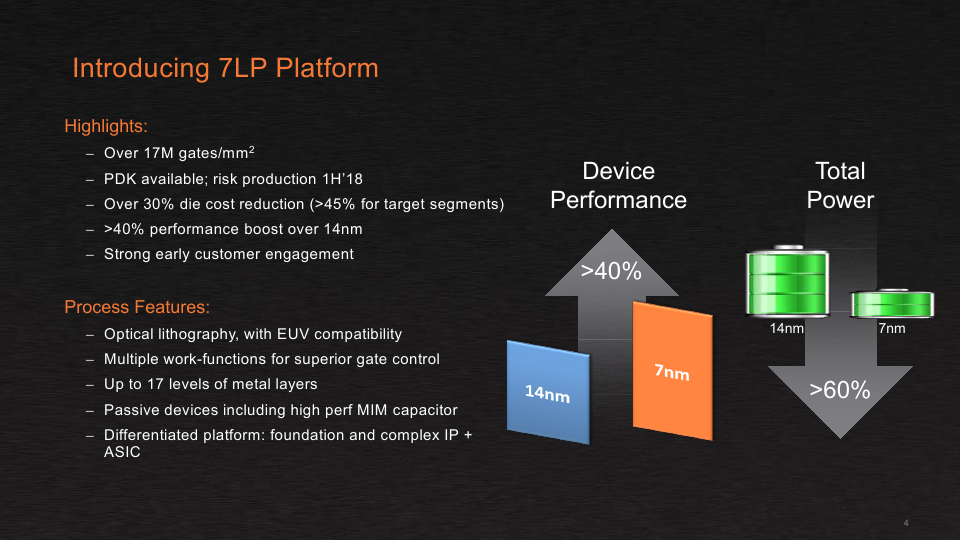

7LP Canned Due to Strategy Shift

GlobalFoundries was on track to tape out its clients’ first chips made using its 7 nm process technology in the fourth quarter of this year, but “a few weeks ago” the company decided to take a drastic, strategic turn, says Gary Patton. The CTO stressed that the decision was made not based on technical issues that the company faced, but on a careful consideration of business opportunities the company had with its 7LP platform as well as financial concerns.

It is noteworthy that when GlobalFoundries first announced its 7LP platform in September 2016, it said that it would start risk production of processors using this technology in early 2018 (PR), which means that the first chips should have been taped out before that. When the company detailed the process in June 2018, it said that it expected to start “volume production ramping in the second half of 2018” (PR), which would be close to impossible if customers taped out their first chips only in Q4.

Generally, it looks like the company had to adjust its roadmap somewhere along the way, moving the start of high-volume manufacturing (HVM) further into 2019. Whether or not these adjustments had any implications on GlobalFoundries is up to debate. Keep in mind that AMD’s first 7 nm product was designed for TSMC’s CLN7FF from the beginning, so the company did not bet on GF’s 7LP in late 2018 anyway, and no rush with the manufacturing technology was needed for GF’s key customer.

Along with the cancellation of the 7LP, GlobalFoundries essentially canned all pathfinding and research operations for 5 nm and 3 nm nodes. The company will continue to work with the IBM Research Alliance (in Albany, NY) until the end of this year, but GlobalFoundries is not sure it makes sense to invest in R&D for ‘bleeding edge’ nodes given that it does not plan to use them any time soon. The manufacturer will continue to cooperate with IMEC, which works on a broader set of technologies that will be useful for GF’s upcoming specialized fabrication processes, but obviously it will refocus its priorities there as well (more on GF’s future process technologies later in this article).

So, the key takeaway here is that while the 7LP platform was a bit behind TSMC’s CLN7FF when it comes to HVM – and GlobalFoundries has never been first to market with leading edge bulk manufacturing technologies anyway – there were no issues with the fabrication process itself. Rather there were deeper economic reasons behind the decision.

![]()

Economic Reasons Behind the Move

As we noted in our article covering GlobalFoundries's new CEO hire earlier this year, former CEO Sanjay Jha was never able to make the company profitable. His key tasks were to increase GlobalFoundries’s sales, streamline the company in general, and ensure that it executes its roadmap.

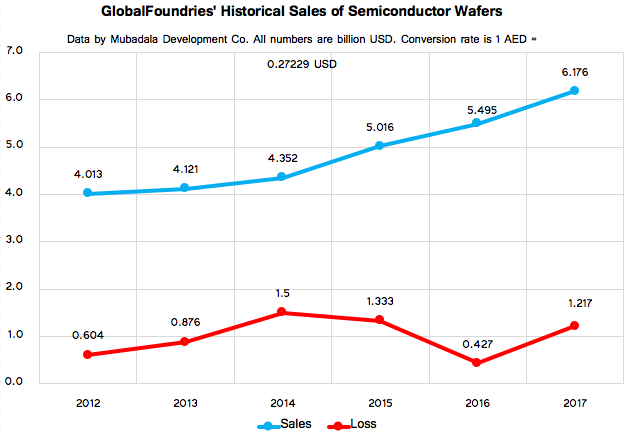

To address the needs of the manufacturer’s traditional key client (AMD) and ensure that his company was competitive against other contract makers of semiconductors, he licensed Samsung Foundry's 14LPP fabrication technology. That strategy worked well. With Sunjay Jha at the helm, GlobalFoundries has managed to land a variety of new customers and increase its sales of semiconductor wafers from approximately $4.121 billion in 2013 to $6.176 billion in 2017. Besides, the foundry’s leading-edge Fab 8, which has been processing wafers using exclusively 14LPP process technology for well over 1.5 years now, is running at full capacity.

To ensure that GlobalFoundries remains competitive against Samsung Foundry and TSMC in the long run, Sunjay Jha obtained IP and development teams from IBM (along with two fabs and a lot of obligations), and poured in billions of dollars in development of the 7LP fabrication technology platform. The latter would include three generations of manufacturing processes and, possibly, a custom high-performance technology available exclusively to IBM. While everything appeared to proceed smoothly with the 1st Gen 7 nm process (DUV only), the 2nd Gen 7 nm process (with EUV used for non-critical layers, such as padding) still needed some additional development investments, and the 3rd Gen 7 nm (with intensive usage of EUV) required even more money for development and further could require installation of additional EUV equipment. Meanwhile, there were two things to consider.

First. If GlobalFoundries kicks off production using the 1st Gen 7 nm fabrication process, it would have needed to cure all of its teething troubles and offer its clients a roadmap forward. The latter would have included 2nd Gen and 3rd Gen 7 nm, but nothing stops there. Customers would have asked for 5 nm and then for 3 nm nodes. Meanwhile, you cannot tell your clients that you are packing up after a certain node and then hope that this node will be a success (the same is true for DUV-only 1st Gen 7 nm).

Second. Development of leading-edge process technologies is extremely expensive. Every new node requires billions of dollars in investments. Those costs are eventually amortized over each chip the company makes, so to keep increasing R&D costs from driving up chip prices, foundries need to produce more chips. To make more chips, they need to either run multiple fabs that use the same process technology (these are going to cost $10+ billion in the EUV era), or build giant fabs that process a gargantuan number of wafers (these are going to cost $20+ billion in the EUV era). Meanwhile, GlobalFoundries has only one leading-edge fab featuring capacity of 60,000 wafer starts per month. As a result, either GlobalFoundries has to pass these R&D costs on to the finite number of wafers it processes – and become uncompetitive against rivals in the process – or eat the costs with reduced profitability.

Meanwhile, having spent well over $20 billion on GlobalFoundries over the last 10 years, Mubadala, the owner of the company, is not inclined to lose more money or invest tens of billions in the hopes of becoming profitable one day. The investor wants GlobalFoundries to stop bleeding and start generating profits.

“The culture of [our investments], the ones I’ve been involved with, was about accumulating assets and then just maintaining it,” said Mubadala CEO Khaldoon Al Mubarak in an interview with Bloomberg earlier this year. “The shift that has happened over the last couple of years, that I’ve tried to push at Mubadala today, is a monetization strategy that makes sense, not with a view to cash out but with a view to reinvest.”

Gary Patton admits that GlobalFoundries never planned to be a leading producer of 7-nm chips in terms of volume. Furthermore, the company has been seeing increasing adoption of its 14LPP/12LP technologies by designers of various emerging devices, keeping Fab 8 busy and leaving fewer step-and-scan systems for 7LP products.

Without another big fab, it would be impossible to make any new leading-edge process technology competitive against Samsung and TSMC due to aforementioned scale reasons. Meanwhile, building a new fab (or even expanding the Fab 8 with another clean room module, which is something that GF considered several years ago) and creating another node or two would require another $10 – $15 billion from Mubadala, which is not inclined to invest just now. As a result, the GlobalFoundries has decided to switch entirely to specialized process technologies for emerging high-growth markets. This strategic shift enables it to reduce spending on R&D, slowdown procurement of new equipment, reduce its workforce by 5% (most of which will be in Malta), and potentially avoid direct competition against the aforementioned contract makers of semiconductors.

127 Comments

View All Comments

FunBunny2 - Tuesday, August 28, 2018 - link

"Oh....the.....horror....."the snark is well done. but... a static socio-economic environment is otherwise called "The Dark Ages". but this one is forever. if Social Darwinism is the paradigm going into the permanent Dark Age, said children's biggest worry won't be the missing electronics that double in speed every few years.

benedict - Tuesday, August 28, 2018 - link

There never was a need to buy a new TV every 4 years. The crazy consumerism making people replace their perfectly working electronics every 1-2 years is a phenomenon almost exclusively happening in the USA and it cannot end soon enough.Believe it or not, life will keep going on after the death of Moore's law.

FMinus - Wednesday, August 29, 2018 - link

I think most people just keep their TVs until they die or the provider does something to make them obsolete, like in my case in 2008 my cable provider decided to kill analog over cable completely, so I had to throw out that CRT TV otherwise I'd still have it for a few more years, but that was a reasonable switch. That flat panel that replaced the LCD is still working in the bedroom, whilst we bought a new TV for the living room somewhere in 2014, and I intend to keep it until it dies, or the standards change and it becomes useless, but that likely wont be happening before it actually dies by itself.V900 - Monday, August 27, 2018 - link

AMD will land on their feet, but this will REALLY suck for IBM who must regret betting the farm (and their fabrication guys on Global Foundries.)And of course, with only 2 fabs doing leading edge work, at some point it could mean delays for everyone who isn’t Apple or Samsung.

nevcairiel - Monday, August 27, 2018 - link

Its really still 3 fabs, TSMC, Samsung and Intel. Maybe Intel will use that chance and do more third-party fabbing.V900 - Monday, August 27, 2018 - link

It’s not as easy as that.It’s not like Intel is running a furniture factory, where anyone can get their table built, if IKEA is taking up all of the production at the usual plant.

(This is also why Intels last attempt at “renting out fab space” went so poorly.

Intels fabrication methods are tied into their design methods. They’re using their own tools and even design things somewhat differently from other companies. (Even AMD).

Intel’s fans and designers are used to a process that’s much more reliant on full-custom hand-crafted circuits which are intimately tied to the process.

Pretty much all of their IP, including the stuff for fabrication is designed and developed in-house, and is sometimes CPU specific.

Compare that to the rest of the industry that mostly uses common tools, and you can see the problem.

Going from TSMC to Samsung with a design might mean a delay of a few months, as you rejig the design to be built on Samsung’s process and tools.

Going from TSMC to Intel would mean a major delay as you redo the design for a process that was designed specifically for Intels needs and internal tools. If the chip is really complex, in some cases it would be easier and faster just to junk your design and start from close to scratch.

zodiacfml - Monday, August 27, 2018 - link

Now it seems that if a fab produces mobile chips, it is more likely to thrive.Comdrpopnfresh - Monday, August 27, 2018 - link

Very interesting. To me, this represents the canary in the silicon mine. Though, I did not expect it as soon as this.Maybe the other foundries will see these changes for what they are- submitting to physics. No sense in expensive pursuits that hasten arriving at the end of the road.

rahvin - Monday, August 27, 2018 - link

I think the writings been the wall for a while. Fab prices have been far exceeding estimates, almost exponential growth in costs is simply unsustainable.ChrisGar15 - Wednesday, August 29, 2018 - link

There is an industry view that mature markets evolve into 3 main players. (with occasional disruptions & consolidations) There is a big player (e.g., 70% market share) ... and 2nd player (20-30% market share) ... and a niche/3rd player.I think the semiconductor market is evolving this way also. (my guess is Samsung will evolve to be the 2nd player -- but we'll see)