Market Trends Q1 2016: Shipments of SSDs Up 32.7% Year-over-Year

by Anton Shilov on May 25, 2016 12:01 PM EST

Shipments of SSDs in the first quarter of 2016 were up 32.7% compared to the same period a year ago, according to findings of TrendFocus*, a storage market tracking company. Sales of all types of SSDs, including those for client and server systems, were up sequentially and year-over-year, which indicates that NAND-based storage devices are taking share away from traditional hard drives.

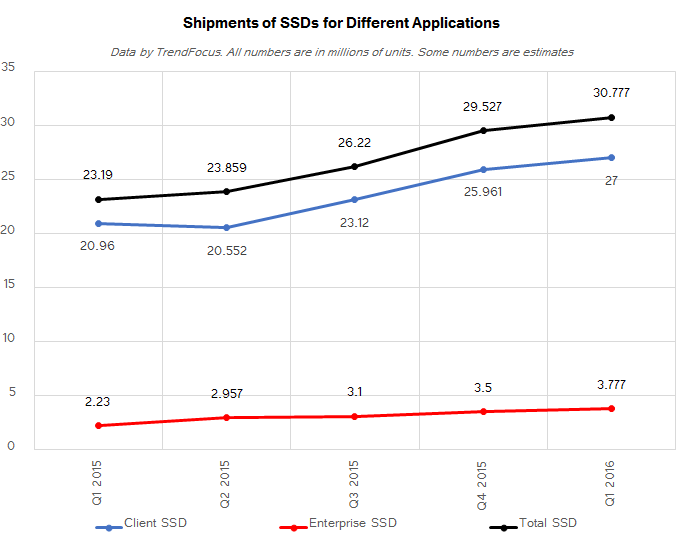

30.777 Million SSDs Shipped in Q1 2016

The industry sold a total of 30.777 million SSDs in Q1 2016, up 32% from 23.190 million in the same period of 2015, according to data by TrendFocus. By contrast, shipments of PCs dropped to 60.6-64.8 million units (according to Gartner and IDC), or by around 10% year-over-year (YoY); whereas shipments of HDDs collapsed by 20% YoY, based on data from hard drive manufacturers. The growth of SSDs has been consistent despite slowing sales of PCs and HDDs for several quarters now, therefore, a minor sequential increase (~4%) of their shipments in Q1 2016 was not surprising.

Of nearly 31 million SSDs sold in the first quarter, approximately 27 million drives were designed for client PCs, whereas about ~4 million were aimed at servers. In the PC space, sales of SSDs grew about 29% over the first quarter of last year, but in the enterprise space shipments of SSDs skyrocketed by 69% compared to the same period in 2015.

TrendFocus estimates that the total capacity of SSDs shipped in Q1 2016 was around 10 Exabytes, up from 5.65 EB in Q1 2015, an increase of nearly 77%. The average capacity of one SSD also grew from approximately 245 GB in the first quarter last year to roughly 325 GB in the first quarter of this year (or by 33%).

Due to speedy development of solid-state drives, there are multiple trends, which help to speed up adoption of NAND flash storage across the whole spectrum of the market. Rapid per-GB price declines thanks to TLC NAND help to reduce prices of entry-level SSDs. As a result, 120 GB solid-state drives now cost only around $40 in retail, which is why many PC makers use them instead of HDDs. In addition, major performance improvements thanks to NVMe and new controllers are driving adoption of SSDs by high-end client computers.

Samsung Remains No. 1 SSD Maker

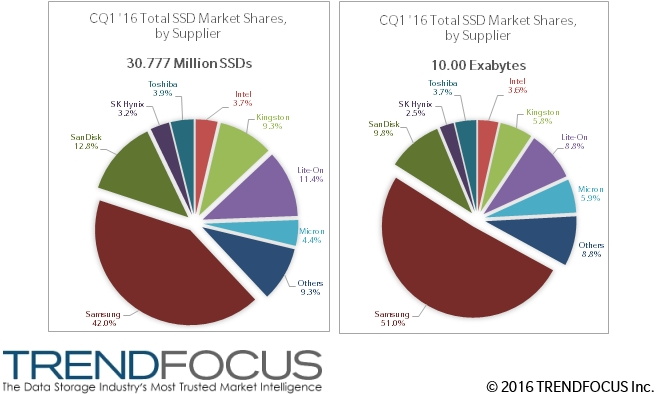

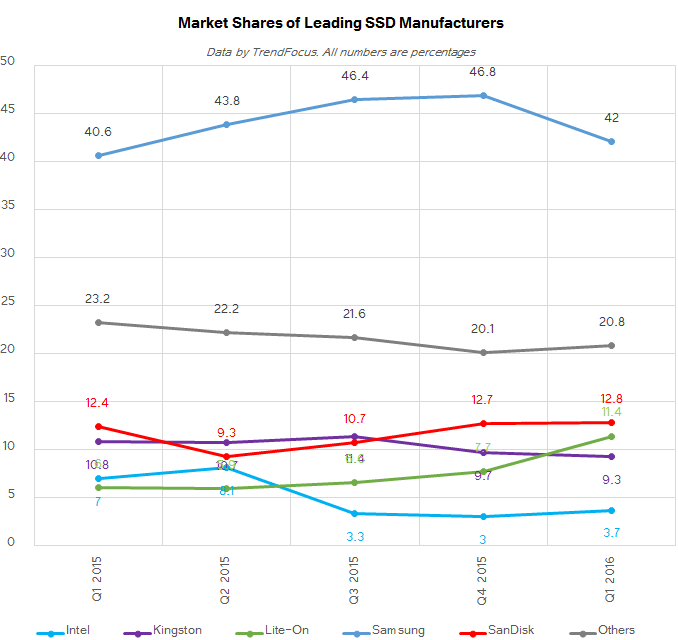

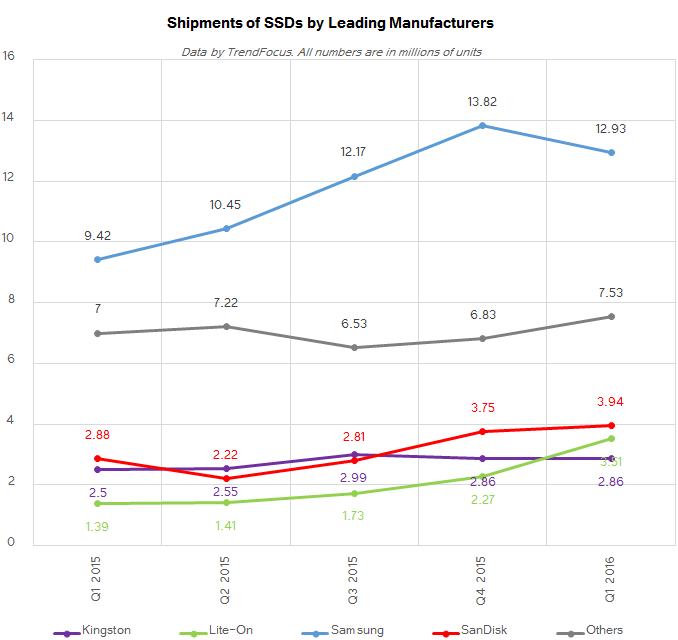

Samsung is the world’s largest maker of NAND flash and is also the largest manufacturer of SSDs. The company has been controlling over 40% of the market for a while now and its unit shipments increased from 9.42 million in Q1 2015 to 12.93 million in Q1 2016. Samsung supplies SSDs to such large PC makers as Apple, HP and Lenovo, therefore, its success is well expected.

The second largest supplier of SSDs in Q1 2016 was SanDisk, which shipped 3.94 million drives and controlled 12.8% of the market. It is noteworthy that while SanDisk and Toshiba operate the world’s largest NAND flash manufacturing complex, the latter is not a major maker of SSDs. In Q1 the company only sold 1.2 million of SSDs, whereas its market share was 3.9%.

The world’s third largest supplier of SSDs in the first quarter of 2016 was Lite-On, which sells drives under Plextor and Lite-On brands. The company not only increased shipments of its SSDs from 1.39 million units in Q1 2015 to 3.51 million units in Q1 2016, or by 152% year-over-year, but also gained a significant amount of market share. In the first quarter Lite-On controlled 11.4% of the global SSD shipments.

Kingston, which is the world’s No. 1 independent supplier of DRAM modules, is also a significant maker of SSDs. The last 12 months were not exactly good for Kingston in comparison to others. Unit sales of Kingston’s SSDs only increased by around 14% year over year, but its market share dropped from 10.8% in Q1 2015 to 9.3% in Q1 2016.

It is noteworthy that shipments and market shares of Intel, Micron and HGST dropped year-over-year. The reasons for that are unclear, but it is possible that the three companies focused on high-capacity enterprise-class SSDs, which is why their unit sales declined.

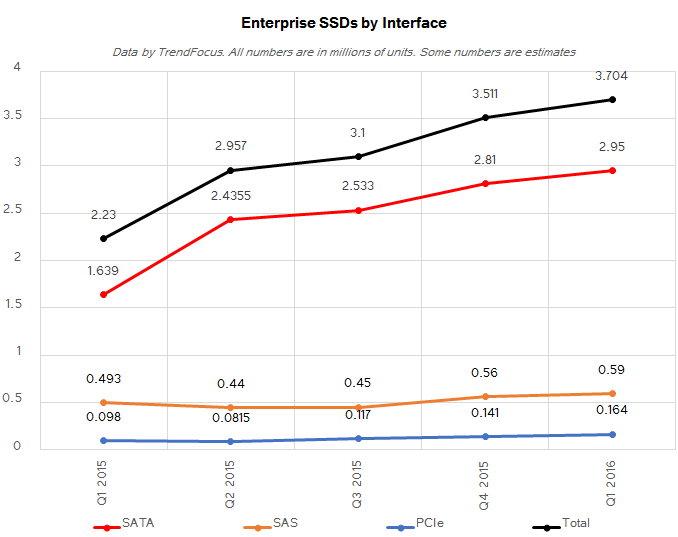

Shipments of PCIe and SAS Enterprise SSDs Are Growing, But Unit Numbers Are Not High

When it comes to data-centers, multiple companies are replacing their 10K/15K HDD-based mission critical deployments with SSDs at a very rapid pace. Since one high-end enterprise SSD offers higher IOPS and throughput than multiple hard drives, volume shipments of PCIe and SAS solid-state drives are not high. In the first quarter only around 164 thousand of PCIe enterprise SSDs were shipped, whereas sales of SAS-based SSDs grew to 590 thousand units. By contrast, the industry sold 2.95 million SSDs with a SATA interface.

TrendFocus believes that Samsung, Intel and HGST control the lion’s share of enterprise SSDs (approximately 80%). HGST is also a leading supplier of enterprise-class HDDs, which is why the transition from HDDs to SSDs by various owners of data-centers does not hurt the company, but rather allows it to capitalize on its SAS expertise.

The Future Looks Bright for SSDs

If sales of PCs drop in Q2 2016, shipments of SSDs and HDDs will decline as well. Earlier this year Western Digital already predicted a slight decrease of the HDD TAM (total available market) in the second quarter, which is a bad news for storage market in general. On the other hand, shipments of PCs usually increase in the second half of the year, which means that not only HDDs 'should' rebound, but SSDs will have good chances to set a new record in terms of unit shipments (we say should, as various reports have mixed predictions).

There are several positive trends for the solid-state storage in general. Firstly, NAND flash is getting cheaper to manufacture and companies like Intel and Micron are about to ramp up production of their 3D NAND. More affordable memory helps to build cheaper SSDs. Secondly, the share of mobile PCs that can only house SSDs is increasing as computers are getting thinner and lighter. Thirdly, Seagate no longer wants to aggressively participate in the market of affordable notebook storage. All-in-all, the future looks good SSDs, but the question is whether all market participants are ready to take advantage of the current situation.

*Please note that some of the numbers mentioned in this news story were not directly revealed by TrendFocus as a part of the company’s press release on the matter, which is why we fetched them from previous announcements, or estimated based on previously released numbers by the company. If you need precise numbers for business decisions, you should acquire the full report from TrendFocus.

Source: TrendFocus

11 Comments

View All Comments

Gunbuster - Wednesday, May 25, 2016 - link

Thank goodness. Cant wait to celebrate the day when the last ever device with a spinning platter boot drive and 720p LCD rolls off the assembly line. Should make it a GD nation holiday IMHO.jasonelmore - Wednesday, May 25, 2016 - link

So HDD shipments down 45% and SSD shipments up 35%. There is still a 10% decline in storage in general.Yojimbo - Wednesday, May 25, 2016 - link

Percentages don't work that way. Assuming your HDD and SSD shipment change percentages are correct/consistent, what you said would only be true if SSD shipments were about 78% of HDD shipments prior to the increase/decrease in shipments.Shadowmaster625 - Wednesday, May 25, 2016 - link

I dont think you can compare the number directly like that. I wish the SSD and HDD data was all on one chart though.name99 - Wednesday, May 25, 2016 - link

The interesting comparison number is thatSSD shipments total about 10 exabytes for the quarter.

31 million units, so mean size of about 320 GB (higher than I would have thought!)

HD shipments total about 150 exabytes for the quarter.

120 million units, so mean size of about 1.25 TB (that sounds about right, when you think of all the large backup drives and the small 500, or 750 GB drives in cheap machines).

http://www.anandtech.com/show/10098/market-views-2...

CaedenV - Thursday, May 26, 2016 - link

that HD number seems rather low to me somehow. I mean, the vast majority of HDDs are sold to companies and data storage providers, and I would think they were all up on 3-4TB drives by now. But with the average so low it must mean a lot of them are still buying 1-2TB drives.Drumsticks - Wednesday, May 25, 2016 - link

Go, SSDs, go!I interned for Intel NSG last year working on a SATA product, and I can definitely say their focus is more on the enterprise market; that probably explains the drop in their overall market share. It's all about margins, and Enterprise is where you can find those in SSDs (even though a good consumer Intel drive would be cool).

digiguy - Wednesday, May 25, 2016 - link

"The growth of SSDs has been consistent despite slowing sales of PCs "Well, SSDs are actually one of the main drivers of slowing PC sales... They have given new life to lots of relatively old but still good enough or even powerful PCs. All my laptops now have one or 2 SSDs.

For instance, instead of buying a new ultrabook, precisely today I invested in a 1TB 850 EVO to replace the (now full) 256GB SSD in my 2012 14-inch ultrabook, which still rocks (i7-2640M with 8 GB RAM). This will allow me to extend its life for many years to come and to create a dual boot windows 7 + windows 10 (for when windows 7 is no longer supported).

Having said that, HDD will still be with us for a very long time as a cheaper data storage solution (2nd drive or external drive), no need to pay a premium to store data....

Phillsco - Thursday, May 26, 2016 - link

What about industrial-grade SSDs sold into commercial/industrial markets, what % of the market are they?zodiacfml - Friday, May 27, 2016 - link

LOL at Seagate